About UAE Corporate Tax:

UAE’s competitive CT regime is based on international best practices and is expected to cement the UAE’s position as a leading global hub for business and investments and accelerate the UAE’s development and transformation to achieve its strategic objectives.

Introduction of a CT regime reaffirms the UAE’s commitment to meeting international standards for tax transparency and preventing harmful tax practices.

The new tax resident definition gives additional clarity to individuals in respect of their UAE tax residency position under bilateral tax agreements the UAE has entered with other territories, many of which refers to the domestic laws of the UAE for determining whether a person is a resident of the UAE for purposes of the treaty.

Natural persons who are UAE Tax Residents would not be subjected to taxation as the UAE does not levy any personal income tax on the employment or other personal income of individuals.

Effective Financial Year:

A business that has a financial year starting on 1 July 2023 and ending on 30 June 2024 will become subject to UAE CT from 1

July 2023 (which is the beginning of the first financial year that starts on or after 1 June 2023).

A business that has a financial year starting on 1 January 2023 and ending on 31 December 2023 will become subject to UAE CT from 1 January 2024 (which is the beginning of the first financial year that starts on or after 1 June 2023).

Applicability:

- Individual:

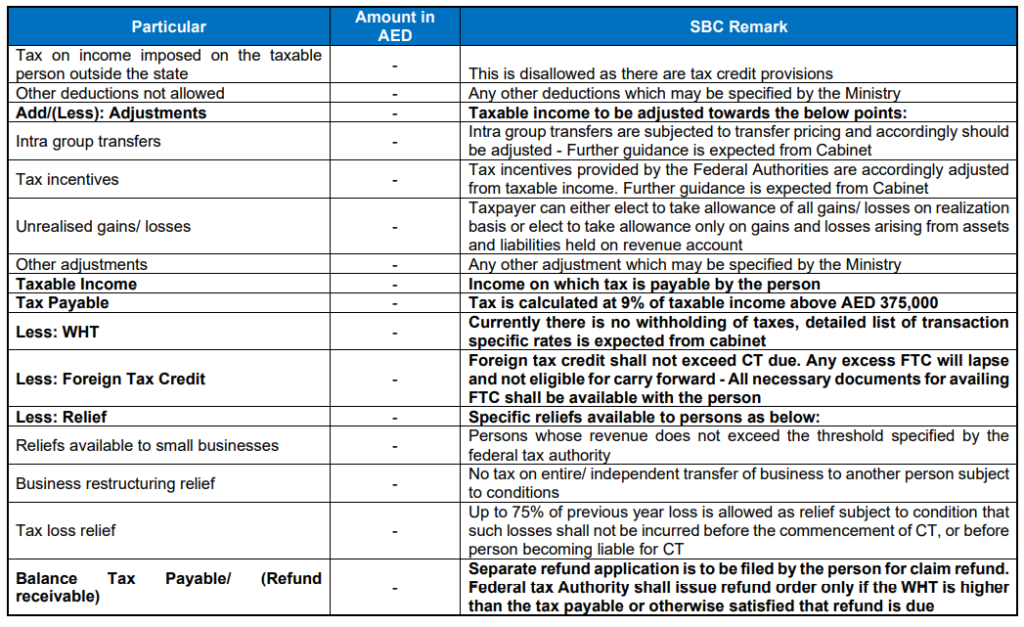

For Individuals and Juridical Persons 0% for taxable income up to and including AED 375,000 (this amount is to be confirmed in a

Cabinet Decision). 9% for taxable income exceeding AED 375,000.

Example:

If the person has Income less than 375,000 AED the tax is 0% for that person. But they need to file returns to exempt the taxable income.

If someone has Income more than 3750,000 AED. They must pay corporate tax regime in UAE.

Taxable Income:

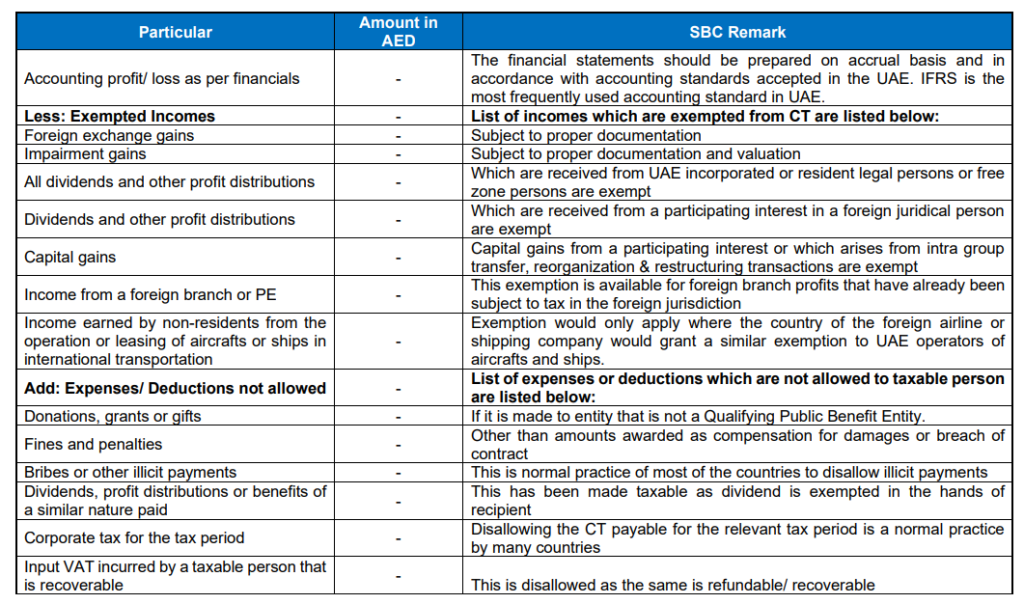

Financial Statements to be prepared as per Accounting Standards accepted in UAE.

• Taxable income for a tax period is determined based on the accounting profit or (loss) after marking adjustments for certain items.

• For UAE CT purposes, financial statements should be prepared in accordance with the accounting standards accepted in the UAE (IFRS is most frequently used accounting standard in the UAE). Accepted Basis of Accounting for computing Taxable Income.

• Taxpayers should prepare the financial statements and determine taxable income on Accrual basis.

• Only certain categories of individuals entrepreneurs and small businesses are allowed to use Cash basis of accounting.

Accounting Net Profit or (Loss) would need to be adjusted for following items for

arriving at the taxable income.

• Exempt Incomes

• Any Incentives / Tax Reliefs

• Deductions not allowable

• TP adjustments Intra-group transfers

• Any other adjustments specified by Ministry.

Exempted Income:

Dividends and other profit distributions received from UAE incorporated or resident legal persons (even where UAE juridical person is subject to 0% Free Zone CT rate).

• Dividends and other profit distributions received from a Participating Interest in a foreign juridical person.

• Certain other income (e.g., capital gains, foreign exchange gains / losses and impairment gains or losses) from a Participating Interest.

• Income from a foreign branch or PE where an election is made to claim the “Foreign Permanent Establishment” exemption.

• Income earned by non-residents from the operation or leasing of aircrafts or ships in international transportation where certain conditions are met.

Registration and Returns:

Registration

All persons liable to tax must obtain a separate registration pursuant to which, the Tax registration number (TRN) will be allotted to such taxable person for making the payment of tax and filing the return.

• To obtain corporate tax exemption, exempt persons or unincorporated partnerships shall apply for registration.

• Automatic registration will take place if Suo-moto not registered.

• At the time of cessation, dissolution, liquidation, merger and amalgamation, taxable person shall apply for deregistration of TRN allotted only after payment of all tax liabilities, if any & filing the pending tax returns.

Returns

Taxable person to file a return within 9 months from the end of the relevant tax period.

• Authorized partner in an unincorporated partnership to be treated as taxable person to submit a declaration.

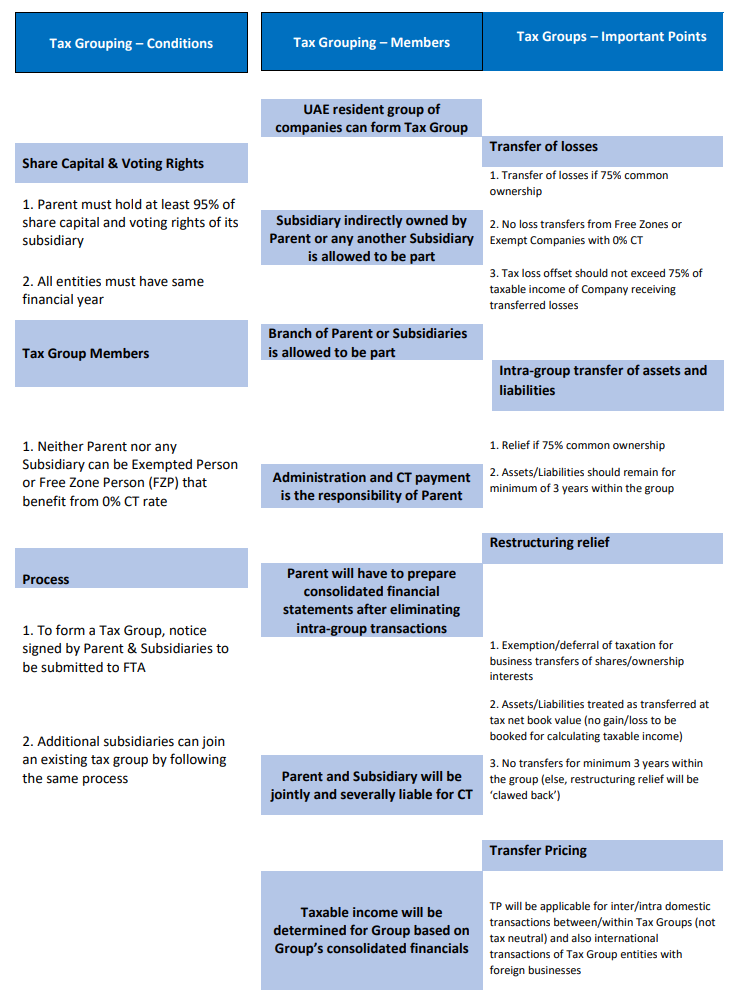

• The parent company to file a tax return on behalf of the tax group.

Indicative Tax Computation Sheet:

Tax Groups:

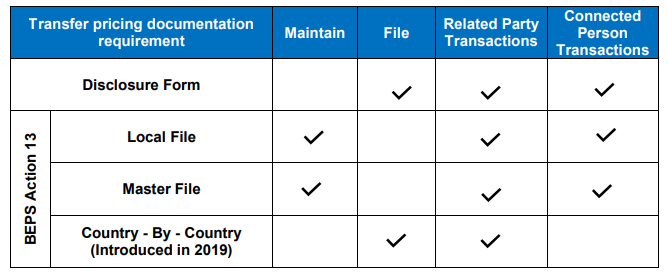

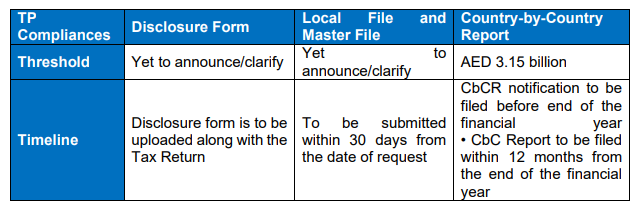

UAE TP Documentation Requirements:

- Businesses will be required to submit a disclosure containing information regarding their transactions with Related Parties and Connected Persons.

- Businesses will also need to maintain a three-tier documentation (Local File, Master File and Country-by-Country Report) in line with OECD BEPS Action 13 requirements, where the arm’s length value of their Related Party Transactions exceeds a certain threshold in the relevant tax period.

• Disclosure Form must be filed along with the Tax Return. Local File and Master File has to be filed within 30 days following a request by the Authority.

• TP is not applicable to Govt Entity, Govt Controlled Entity, Extractive and Non – Extractive Natural Resource Business.

Arm`s Length Principle:

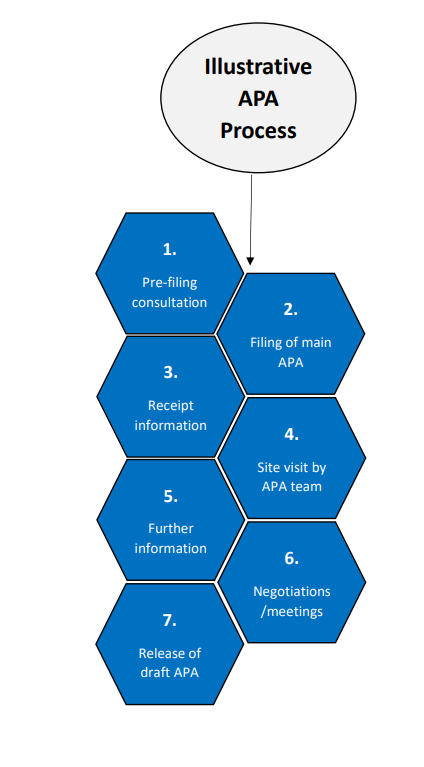

Advance Pricing Agreement (APA) – Introduced.

• Alternative Dispute Resolution Mechanism to obtain TP certainty on existing/proposed inter-company transactions.

• UAE CT Law incorporates APA regime like other jurisdictions.

• APA application process and the manner of APA site visit, re-negotiation and signing is to be prescribed by FTA.